Blog > Why More Parents Are Helping Their Kids Buy Homes Instead of Paying for College

Why More Parents Are Helping Their Kids Buy Homes Instead of Paying for College

by

Owning a home has always been a big part of the American dream. It’s one of the main ways people build long-term wealth. But right now, for younger buyers, getting into a home is harder than it used to be. Rising home prices, higher mortgage rates, inflation, and student debt are all making it tougher to buy. Because of this, first-time buyers are getting older, and many are struggling to take that first step. As a result, more parents are stepping in to help.

A recent study found that 74% of parents would consider helping their child buy a home, and nearly 29% say helping with a home purchase is more important than paying for college. This marks a big shift from the past, when most families focused mainly on saving for education. Now, many are starting to see homeownership as just as important, if not more important, for long-term financial stability.

There are a few key reasons behind this change. First, it’s simply harder to buy a home today. Mortgage rates have climbed, and saving for a down payment has become one of the biggest challenges for young buyers. At the same time, student loan debt is still a major issue, making it harder for many people to save or qualify for a mortgage. These financial pressures are forcing families to rethink where their support can make the biggest impact.

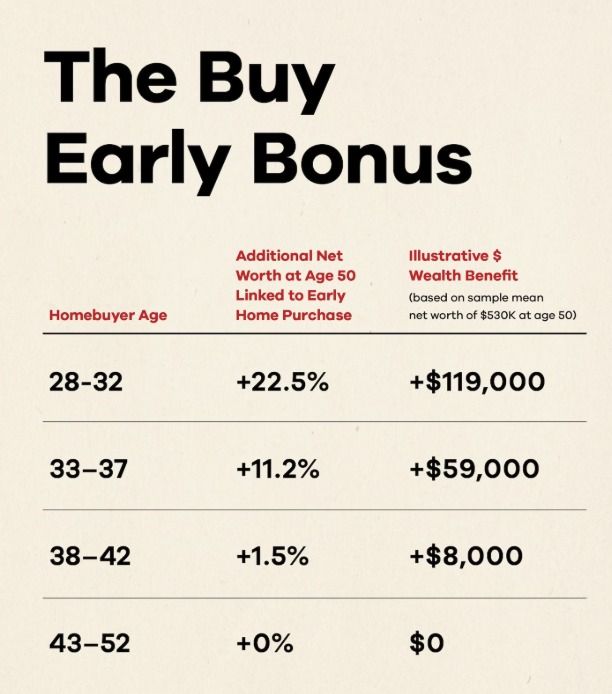

Another major reason comes down to timing. Research shows that buying a home earlier in life can lead to significantly higher net worth later on. People who purchase a home by age 30 tend to have more wealth by age 50 compared to those who wait until their 40s. This is because they have more time to build equity and benefit from rising home values.

Some families are finding creative ways to help without directly giving money. For example, some parents allow their children to live at home longer or help cover living expenses so they can save faster. This kind of support can make a big difference, helping young buyers enter the market sooner and with more confidence. In many cases, becoming a homeowner also helps people grow financially and take on more responsibility.

There has also been a broader shift in how people view college. Compared to years ago, student debt is higher, career paths are more flexible, and there is growing demand for skilled trades. Technology and changes in the job market are also reshaping how people think about education. Because of this, families are taking a closer look at where their money will have the greatest long-term impact.

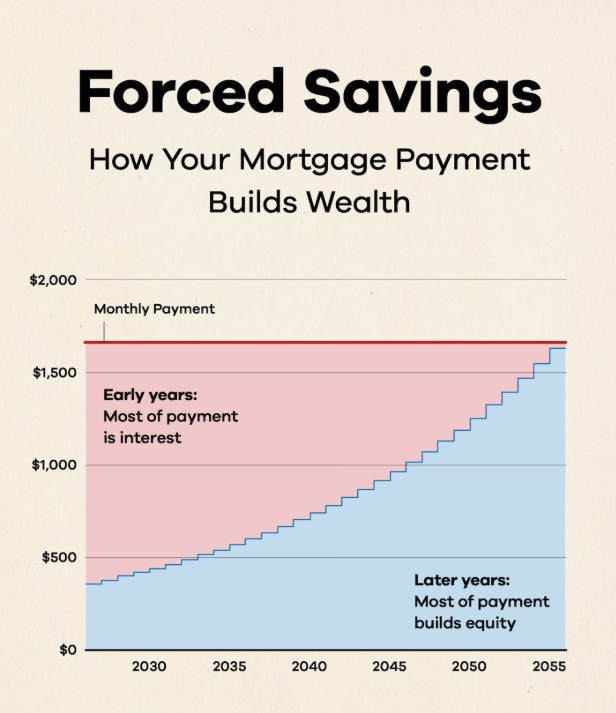

Helping a child buy a home earlier can be a powerful financial move. It allows them to start building equity sooner, stabilize their housing costs, and grow wealth over time. Even a small contribution toward a down payment can change their financial path in a meaningful way.

This trend is also having an impact on the housing market. First-time buyers play a key role in keeping the market moving. When they are able to purchase homes, it allows current homeowners to sell and move up, creating activity across all price points. Without entry-level buyers, the entire system slows down.

To make this work, many families are getting creative. Some parents are co-signing on loans, offering interest-free loans, giving down payment gifts, or even purchasing a home and renting it to their child until they can take over the mortgage. These strategies are helping bridge the gap where many buyers are struggling.

That said, one challenge still remains: mortgage rates. Even with help from family, higher rates can significantly impact monthly payments. For example, a $300,000 loan today can cost hundreds more per month compared to lower-rate years. So while support helps, it doesn’t completely remove affordability challenges.

When it comes to balancing college savings and helping with a home purchase, there isn’t one right answer. Some families use 529 plans for education, while others prefer more flexible savings options like brokerage accounts. Often, a mix of both works best. The most important thing is having a plan and starting early.

At the same time, parents need to make sure they are still protecting their own financial future, especially when it comes to retirement. Helping the next generation is important, but it shouldn’t come at the cost of their own stability.

In the end, more families are starting to view homeownership as a key part of long-term financial planning. Helping a child buy a home earlier can build confidence, create stability, and open the door to future wealth. But every situation is different, and the best approach depends on your goals, your finances, and your timeline.

If you’re thinking about buying, or helping a family member take that step, it’s worth having a conversation about what makes the most sense in today’s market.